First Light News: The ‘TACO’ that keeps on giving

A month in, and frankly, no one seems any the wiser. The Middle East conflict has entered its fifth week, and we are left with mixed messages.

The Strait of Hormuz – a key waterway through which a fifth of the world’s seaborne oil flows – remains all but impassable, gas pump prices are on the rise, and Trump appears to be running foreign policy through his Truth Social feed. Suffice it to say, it was an interesting week.

The ceasefire that was not, or was it?

You will recall that last week opened with a risk-off phase – equities and Treasuries fell, USD and oil rose. President Trump stepped in and saved the day, delivering his first 5-day extension, citing ‘productive conversations’. Markets ate well that day, and TACOs sold out, leading to risk-on positioning and a relief rally into the close.

What was interesting was that Tehran denied that talks were underway, despite the White House stating that progress was being made. It got to a point where you were questioning both sides’ credibility – a difficult trading environment, to say the least.

What followed was a week of back-and-forth between reality and hope. Last Thursday comes around, and with oil prices already back on the front foot, Trump steps in once more – this time announcing a second extension, adding 10 days to the deadline and bringing it to 6 April. Markets clearly did not buy into this, and TACOs were effectively on sale at the tail end of the week. In a Truth Social post, Trump cited that this extension was due to an ‘Iranian government request’ and added that talks were still ‘going very well’. I am uncertain who Trump’s team is negotiating with, and Iran even went as far as to say that the US is negotiating with itself.

Energy prices, for the most part, largely overlooked Trump’s late-week attempts at de-escalation. Brent Crude spot prices settled firmly back above US$100/barrel, up 6.2% at the close last Friday to US$106.30, with WTI spot ending last week considerably off worst levels and just inching back above US$100 to US$101.17. Should oil remain elevated, this does not bode well for stocks, as high oil prices function as a tax on nearly every aspect of economic activity, and stocks are reflecting this. For equities to gain a foothold, oil prices must drop.

Equities remained broadly range-bound until mid-week, then sold off heavily at the tail-end. The Nasdaq 100 is now well into correction territory and finished the week down 3.2%, along with the Nasdaq Composite and the Dow Jones, which declined by 3.2% and 0.9%, respectively. The S&P 500 is also on the doorstep of correction territory.

‘Negotiating with bombs’

Mid-week saw President Trump’s 11th Cabinet meeting, and it was quite the spectacle. One of the most eye-opening comments came from Pete Hegseth – the Secretary of War – who let us all know that the ‘US was negotiating with bombs’. Aside from the obvious humanitarian impact associated with that remark, what an absurd thing to say from a top government official. One wonders whether anyone pointed this out to him in the White House.

Regarding the ‘gift’ that Trump received from Tehran, which the President referenced with considerable enthusiasm, it turned out to be a handful of vessels that were allowed to pass through the Strait. While a modest gesture if this was indeed the case, Trump interpreted this as something of a diplomatic green light.

Adding further texture to the proceedings, the US is reportedly considering dispatching an additional 10,000 soldiers to the region. This is on top of approximately 5,000 marines already on their way. So, if, as Trump has repeatedly claimed, the war is complete and Iran has been ‘decimated’, one would be forgiven for asking why the US is sending troops? Was the additional 10-day extension simply to provide the US some ‘military breathing room’?

The week that is: Geopolitics and US jobs data front and centre

It is expected to remain a tricky market environment to trade this week. Naturally, the focus will be on developments surrounding the war in the Middle East. Traders are expressing caution, given that the conflict is playing out longer than expected, and the uncertainty around it is keeping market participants on edge. Investors do not like what they see and want a clear resolution, which would trigger a sharp risk rebound and pull the USD and yields southbound.

As I am sure you have seen, the conventional hedges have not proven effective. Treasuries failed to provide much in the way of refuge this month, offering a distinct bear flattening in the yield curve – short-dated maturities rose faster than longer-dated yields. Furthermore, gold has delivered very little and has dropped an eye-popping 15% so far this month, with the CHF and JPY presenting a similar picture. The USD, however, has outperformed, up 2.6% per the USD index.

While economic data has somewhat taken a back seat, the primary macro driver this week will be the US March employment report on Friday. This follows a broadly positive January release, followed by February coming in soft. One good thing here is that the March report is free of disruptions from the government shutdown and will be released on time.

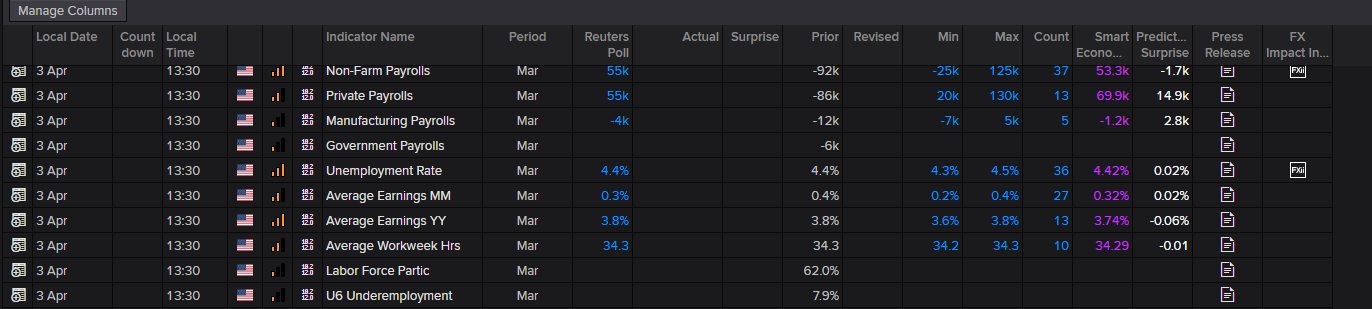

As shown in the LSEG calendar below, expectations suggest a rebound in job growth to 55,000 from a loss of 92,000 positions in February, with private payrolls pretty much echoing a similar picture: 55,000 expected versus 86,000 prior. However, it is worth noting that the min/max estimate range is broad for both, indicating that economists are uncertain heading into this print. Unemployment is forecast to remain steady at 4.4%, while MM average earnings are expected to ease to 0.3% from 0.4%, with the YY measures anticipated to hold at 3.8%.

A month in, and frankly, no one seems any the wiser. The Middle East conflict has entered its fifth week, and we are left with mixed messages.

The Strait of Hormuz – a key waterway through which a fifth of the world’s seaborne oil flows – remains all but impassable, gas pump prices are on the rise, and Trump appears to be running foreign policy through his Truth Social feed. Suffice it to say, it was an interesting week.

The ceasefire that was not, or was it?

You will recall that last week opened with a risk-off phase – equities and Treasuries fell, USD and oil rose. President Trump stepped in and saved the day, delivering his first 5-day extension, citing ‘productive conversations’. Markets ate well that day, and TACOs sold out, leading to risk-on positioning and a relief rally into the close.

What was interesting was that Tehran denied that talks were underway, despite the White House stating that progress was being made. It got to a point where you were questioning both sides’ credibility – a difficult trading environment, to say the least.

What followed was a week of back-and-forth between reality and hope. Last Thursday comes around, and with oil prices already back on the front foot, Trump steps in once more – this time announcing a second extension, adding 10 days to the deadline and bringing it to 6 April. Markets clearly did not buy into this, and TACOs were effectively on sale at the tail end of the week. In a Truth Social post, Trump cited that this extension was due to an ‘Iranian government request’ and added that talks were still ‘going very well’. I am uncertain who Trump’s team is negotiating with, and Iran even went as far as to say that the US is negotiating with itself.

Energy prices, for the most part, largely overlooked Trump’s late-week attempts at de-escalation. Brent Crude spot prices settled firmly back above US$100/barrel, up 6.2% at the close last Friday to US$106.30, with WTI spot ending last week considerably off worst levels and just inching back above US$100 to US$101.17. Should oil remain elevated, this does not bode well for stocks, as high oil prices function as a tax on nearly every aspect of economic activity, and stocks are reflecting this. For equities to gain a foothold, oil prices must drop.

Equities remained broadly range-bound until mid-week, then sold off heavily at the tail-end. The Nasdaq 100 is now well into correction territory and finished the week down 3.2%, along with the Nasdaq Composite and the Dow Jones, which declined by 3.2% and 0.9%, respectively. The S&P 500 is also on the doorstep of correction territory.

‘Negotiating with bombs’

Mid-week saw President Trump’s 11th Cabinet meeting, and it was quite the spectacle. One of the most eye-opening comments came from Pete Hegseth – the Secretary of War – who let us all know that the ‘US was negotiating with bombs’. Aside from the obvious humanitarian impact associated with that remark, what an absurd thing to say from a top government official. One wonders whether anyone pointed this out to him in the White House.

Regarding the ‘gift’ that Trump received from Tehran, which the President referenced with considerable enthusiasm, it turned out to be a handful of vessels that were allowed to pass through the Strait. While a modest gesture if this was indeed the case, Trump interpreted this as something of a diplomatic green light.

Adding further texture to the proceedings, the US is reportedly considering dispatching an additional 10,000 soldiers to the region. This is on top of approximately 5,000 marines already on their way. So, if, as Trump has repeatedly claimed, the war is complete and Iran has been ‘decimated’, one would be forgiven for asking why the US is sending troops? Was the additional 10-day extension simply to provide the US some ‘military breathing room’?

The week that is: Geopolitics and US jobs data front and centre

It is expected to remain a tricky market environment to trade this week. Naturally, the focus will be on developments surrounding the war in the Middle East. Traders are expressing caution, given that the conflict is playing out longer than expected, and the uncertainty around it is keeping market participants on edge. Investors do not like what they see and want a clear resolution, which would trigger a sharp risk rebound and pull the USD and yields southbound.

As I am sure you have seen, the conventional hedges have not proven effective. Treasuries failed to provide much in the way of refuge this month, offering a distinct bear flattening in the yield curve – short-dated maturities rose faster than longer-dated yields. Furthermore, gold has delivered very little and has dropped an eye-popping 15% so far this month, with the CHF and JPY presenting a similar picture. The USD, however, has outperformed, up 2.6% per the USD index.

While economic data has somewhat taken a back seat, the primary macro driver this week will be the US March employment report on Friday. This follows a broadly positive January release, followed by February coming in soft. One good thing here is that the March report is free of disruptions from the government shutdown and will be released on time.

As shown in the LSEG calendar below, expectations suggest a rebound in job growth to 55,000 from a loss of 92,000 positions in February, with private payrolls pretty much echoing a similar picture: 55,000 expected versus 86,000 prior. However, it is worth noting that the min/max estimate range is broad for both, indicating that economists are uncertain heading into this print. Unemployment is forecast to remain steady at 4.4%, while MM average earnings are expected to ease to 0.3% from 0.4%, with the YY measures anticipated to hold at 3.8%.

This will also be the last vital employment number before the next Fed decision on 29 April. While this report may give investors the opportunity to further price in Fed rate path expectations, how the USD ultimately trades depends on the Middle East. If we get another bad jobs number this week, however, it could prompt a dovish Fed repricing and may tame some of the USD’s recent buying. That said, a better-than-expected jobs number would not only allow the Fed to focus more on the inflation side of its mandate but also likely boost current demand for the USD.

We will also have a couple of inflation prints to work with before the next Fed decision, with the next PCE and CPI prints out on 9 and 10 April, respectively, which is arguably more important given the war. Headline inflation is likely to tick higher due to rising oil prices. In most developed markets, interest rate pricing curves have shifted toward a more hawkish stance than a month ago.

You will recall from the last Fed meeting that the central bank kept the target range steady at 3.50-3.75%, and the accompanying rate statement noted that ‘job gains have remained low’, and that ‘the unemployment rate has been little changed in recent months’. This replaced January’s sentence: ‘the unemployment rate has shown some signs of stabilisation’. The latest statement signals that the Fed is growing more concerned about the employment side of its mandate.

Importantly, Fed Chairman Jerome Powell also recently noted that the breakeven rate for employment is ‘very, very low […] you can say the breakeven is zero’. This is the rate at which the US economy must add jobs in order to keep unemployment stable – so not improving or worsening, just treading water. The key takeaway from the breakeven estimates I have seen is that they have fallen dramatically from around 150,000 a few years ago, though there is genuine divergence over how low this bar is set. For example, the St. Louis Fed’s current range is 15,000-87,000 jobs/month, while RBC estimates that the breakeven pace of monthly job growth in 2026 is exceptionally low, at 0-30,000 jobs/month. What this means is that the labour market can essentially tread water at levels that would previously have been considered alarming.

FX outlook for the week ahead:

USD: The USD should remain bid, with traders buying dips amid safe-haven flows. Naturally, a resolution in the Middle East, or signs of progress in any peace talks, could hinder upside in the buck.

GBP: Fundamentals indicate a bearish bias – weak growth, elevated inflation, a loosening jobs market, and dependency on energy. However, BoE rate pricing specifies nearly three rate hikes (68 bps) by year-end, though this could be unwound quickly if a resolution in the Middle East occurs soon.

Euro: It is not a pleasant picture for Europe’s shared currency, weighed by a clear downtrend, meagre growth outlook, and the brutal reality that Europe is a net importer of energy. However, we do have the March eurozone CPI inflation print landing on Tuesday, with a hotter-than-expected reading potentially reinforcing the hawkish ECB pricing (76 bps of tightening by year-end) and offering the EUR some temporary relief, while a soft print could unwind some hawkish bets and deepen the sell-off.

JPY: Japan is in a similar situation to Europe as an energy importer, and with the currency overstretched to the downside and USD/JPY treading water in intervention territory, a short squeeze could soon materialise. Therefore, while USD/JPY longs are clearly still the order of the day per the technical uptrend, caution is warranted.

AUD: While fundamentally, the bias for the AUD remains tilted to longs – bolstered by a hawkish RBA (70 bps of tightening priced by year-end) and being an energy exporter – we must remember the AUD’s risk asset disposition, and positioning is notably crowded long, meaning that it is still very much vulnerable to the downside.

CAD: Although there is clearly an energy tailwind behind the CAD, COT data shows a crowded long CAD position, and the USD is winning the safe-haven bid right now, hence the USD/CAD rallying for five straight days last week. Consequently, the energy story is real; the entry is not, and this may deter CAD longs at current levels unless, of course, there is a strong sign of resolution in the Middle East.

Written by FP Markets Chief Market Analyst Aaron Hill

This will also be the last vital employment number before the next Fed decision on 29 April. While this report may give investors the opportunity to further price in Fed rate path expectations, how the USD ultimately trades depends on the Middle East. If we get another bad jobs number this week, however, it could prompt a dovish Fed repricing and may tame some of the USD’s recent buying. That said, a better-than-expected jobs number would not only allow the Fed to focus more on the inflation side of its mandate but also likely boost current demand for the USD.

We will also have a couple of inflation prints to work with before the next Fed decision, with the next PCE and CPI prints out on 9 and 10 April, respectively, which is arguably more important given the war. Headline inflation is likely to tick higher due to rising oil prices. In most developed markets, interest rate pricing curves have shifted toward a more hawkish stance than a month ago.

You will recall from the last Fed meeting that the central bank kept the target range steady at 3.50-3.75%, and the accompanying rate statement noted that ‘job gains have remained low’, and that ‘the unemployment rate has been little changed in recent months’. This replaced January’s sentence: ‘the unemployment rate has shown some signs of stabilisation’. The latest statement signals that the Fed is growing more concerned about the employment side of its mandate.

Importantly, Fed Chairman Jerome Powell also recently noted that the breakeven rate for employment is ‘very, very low […] you can say the breakeven is zero’. This is the rate at which the US economy must add jobs in order to keep unemployment stable – so not improving or worsening, just treading water. The key takeaway from the breakeven estimates I have seen is that they have fallen dramatically from around 150,000 a few years ago, though there is genuine divergence over how low this bar is set. For example, the St. Louis Fed’s current range is 15,000-87,000 jobs/month, while RBC estimates that the breakeven pace of monthly job growth in 2026 is exceptionally low, at 0-30,000 jobs/month. What this means is that the labour market can essentially tread water at levels that would previously have been considered alarming.

FX outlook for the week ahead:

USD: The USD should remain bid, with traders buying dips amid safe-haven flows. Naturally, a resolution in the Middle East, or signs of progress in any peace talks, could hinder upside in the buck.

GBP: Fundamentals indicate a bearish bias – weak growth, elevated inflation, a loosening jobs market, and dependency on energy. However, BoE rate pricing specifies nearly three rate hikes (68 bps) by year-end, though this could be unwound quickly if a resolution in the Middle East occurs soon.

Euro: It is not a pleasant picture for Europe’s shared currency, weighed by a clear downtrend, meagre growth outlook, and the brutal reality that Europe is a net importer of energy. However, we do have the March eurozone CPI inflation print landing on Tuesday, with a hotter-than-expected reading potentially reinforcing the hawkish ECB pricing (76 bps of tightening by year-end) and offering the EUR some temporary relief, while a soft print could unwind some hawkish bets and deepen the sell-off.

JPY: Japan is in a similar situation to Europe as an energy importer, and with the currency overstretched to the downside and USD/JPY treading water in intervention territory, a short squeeze could soon materialise. Therefore, while USD/JPY longs are clearly still the order of the day per the technical uptrend, caution is warranted.

AUD: While fundamentally, the bias for the AUD remains tilted to longs – bolstered by a hawkish RBA (70 bps of tightening priced by year-end) and being an energy exporter – we must remember the AUD’s risk asset disposition, and positioning is notably crowded long, meaning that it is still very much vulnerable to the downside.

CAD: Although there is clearly an energy tailwind behind the CAD, COT data shows a crowded long CAD position, and the USD is winning the safe-haven bid right now, hence the USD/CAD rallying for five straight days last week. Consequently, the energy story is real; the entry is not, and this may deter CAD longs at current levels unless, of course, there is a strong sign of resolution in the Middle East.

Written by FP Markets Chief Market Analyst Aaron HillPublication date:

2026-03-30 10:53:38 (GMT)